Assessment of business plans, corporate acquisitions or disposals and refinancing will all require due diligence investigations to confirm the facts being represented in the matter under consideration. This will require a tool or series of tools which allow an independent audit of the information being presented so that it may be confirmed in both hard factual and reasonable projection terms.

The history of directorships and the inter-relatedness of companies need to be confirmed so that the question of who is being dealt with is covered. It can also be very illuminating to view the other directorships and shareholdings an individual has. Following the links by director to other companies where the same individual is also a director and following parent subsidiary holdings can often reveal unexpected interrelationships and cross holdings across competitors and sectors. The performance of these related companies is also often instructive.

Analysis of the sector the company is a part of is another key component of due diligence. Industry rankings of turnover and profitability will for example quickly show if claims made in prospectuses stand up. It is very easy to say “we are number 1” in the sector for example but the appropriate industry sector report will confirm or refute this very easily. Market share claims and the size of the market served should be checked from the figures available in a suitable sector report.

Often it is best to refine a listing from a sector report and the analysis is best completed using a shortlist of actual competitors rather than a listing based on SIC classification. The focus of the averages will be dependent on the group of companies used to calculate the benchmarks and as usual it is the same old story : rubbish in rubbish out. In other words the closer the competitors are defined and selected the more useful the comparative analysis. Trends and averages for the relevant sector are a key indicator of future prospects and should be used to inform the investigation – it is very much better if there is knowledge of just what is being averaged to produce these benchmarks when relying on them in this way.

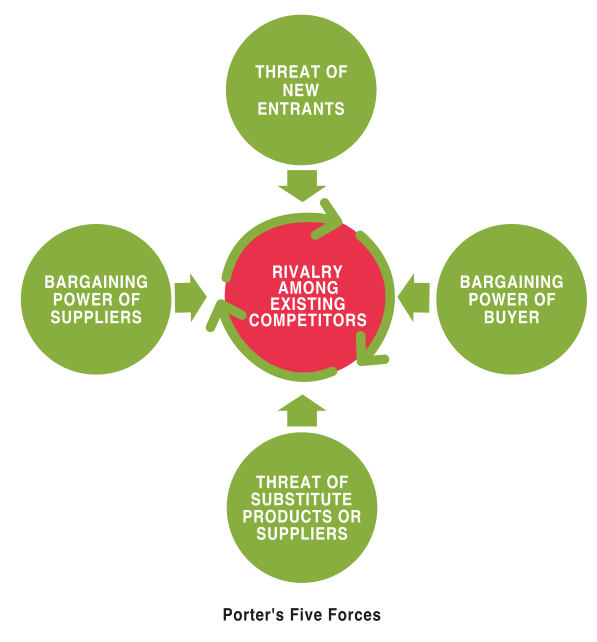

This is true in all the sectors relevant to the firms so a thorough analysis might involve using a model from Micheal Porter looking at buyers, suppliers, substitutes, new entrants as well as the competitors. The power of Porter’s model is that it offers a strategic analysis of the market and goes to the value of the proposition. At the very least it would be sensible to compare the assumptions made in the projections being investigated with what has historically been achieved by well managed firms in the sector. It is perhaps unsurprising that accounts can be manipulated in the short term by deferring costs and pulling forward revenues for example. This can usually be spotted with a cash flow analysis. It would also be clear that ratios from the firm diverged from industry average benchmarks which might be expected.

A good, tightly defined grouping of firms will also provide the most useful ratios and trends for the relevant sub-sector within an industry. So for example an overall industry report might show unspectacular trends for some 600 firms operational in that sector. However, focusing on the 15 or 20 relevant most similar competitors either by size or product or geography for example there might be very interesting trends which can be verified. Within any sector of 600 firms there will be likely to be firms growing, stagnating and declining so the facility to focus more exactly will produce a much clearer picture of the potential.

Conclusion

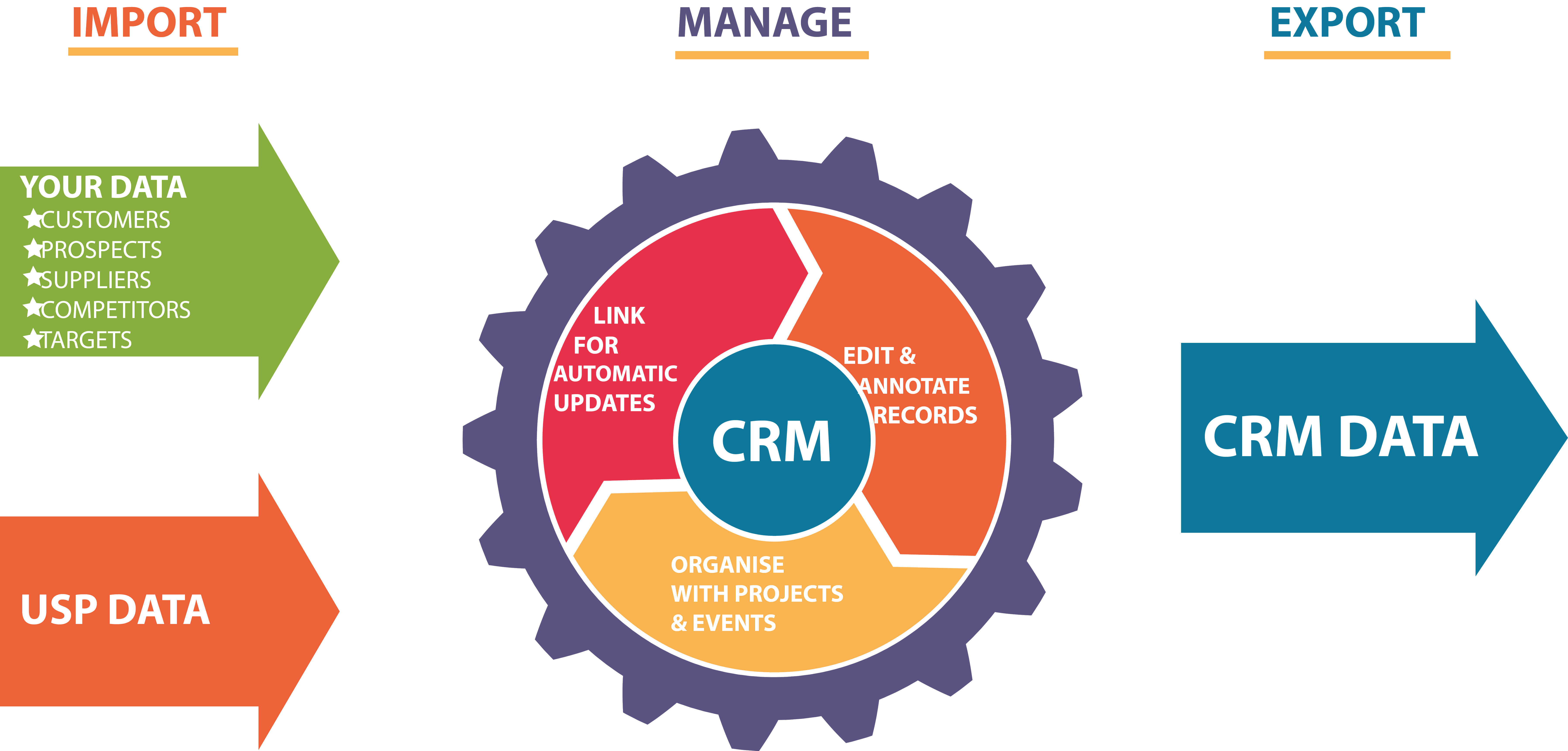

A tool such as USP Data which contains all the live Companies House data linked up to allow directorships and ownership of firms together with the focused industry averages covering all UK sectors will be very helpful for Due Diligence checks. The particular strength of USP is the custom reporting facility which allows the focus on relevant sub-groups within any sector grouping with the associated rankings and averages of relative performance.

Contact us now to find out how USP Data can make your due diligence work easier

Latest articles

Enhancing Acquisition Success through Effective Business Segmentation

In the dynamic landscape of mergers and acquisitions (M&A), the process of business segmentation emerges as a critical component for identifying and evaluating potential targets. Business segmentation within the context of acquisitions involves the strategic categorization of target companies based on various criteria such as financial performance, geographic presence, industry sector, and shareholder profile. This…

Continue reading...Maximizing Business-to-Business Market Segmentation with Comprehensive Data

Understanding your target market is crucial for success in today’s ever-changing business environment. For B2B companies, effective market segmentation serves as the cornerstone of strategic decision-making and customer engagement. However, achieving precision targeting requires more than just surface-level insights. It demands leveraging comprehensive data, including researched industry sector reports, to optimize Business to Business market…

Continue reading...Leveraging Industry-Leading Firmographic Data Selections for Efficient Business Segmentation

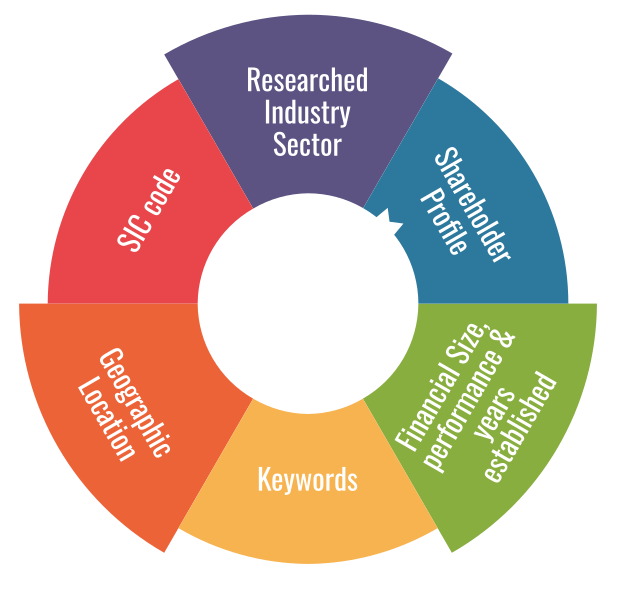

Business segmentation plays a crucial role in tailoring marketing strategies, identifying target markets, and optimising resource allocation. However, the sheer volume of available data can overwhelm businesses, making it challenging to extract actionable insights efficiently. In this context, leveraging industry-leading firmographic data selections, encompassing SIC codes, researched listings, financial parameters, geographic parameters, keywords, and shareholder…

Continue reading...Enhancing Accuracy in Target Market and Market Segmentation: The Superiority of Researched Industry Sector Listings Over SIC Code Classifications

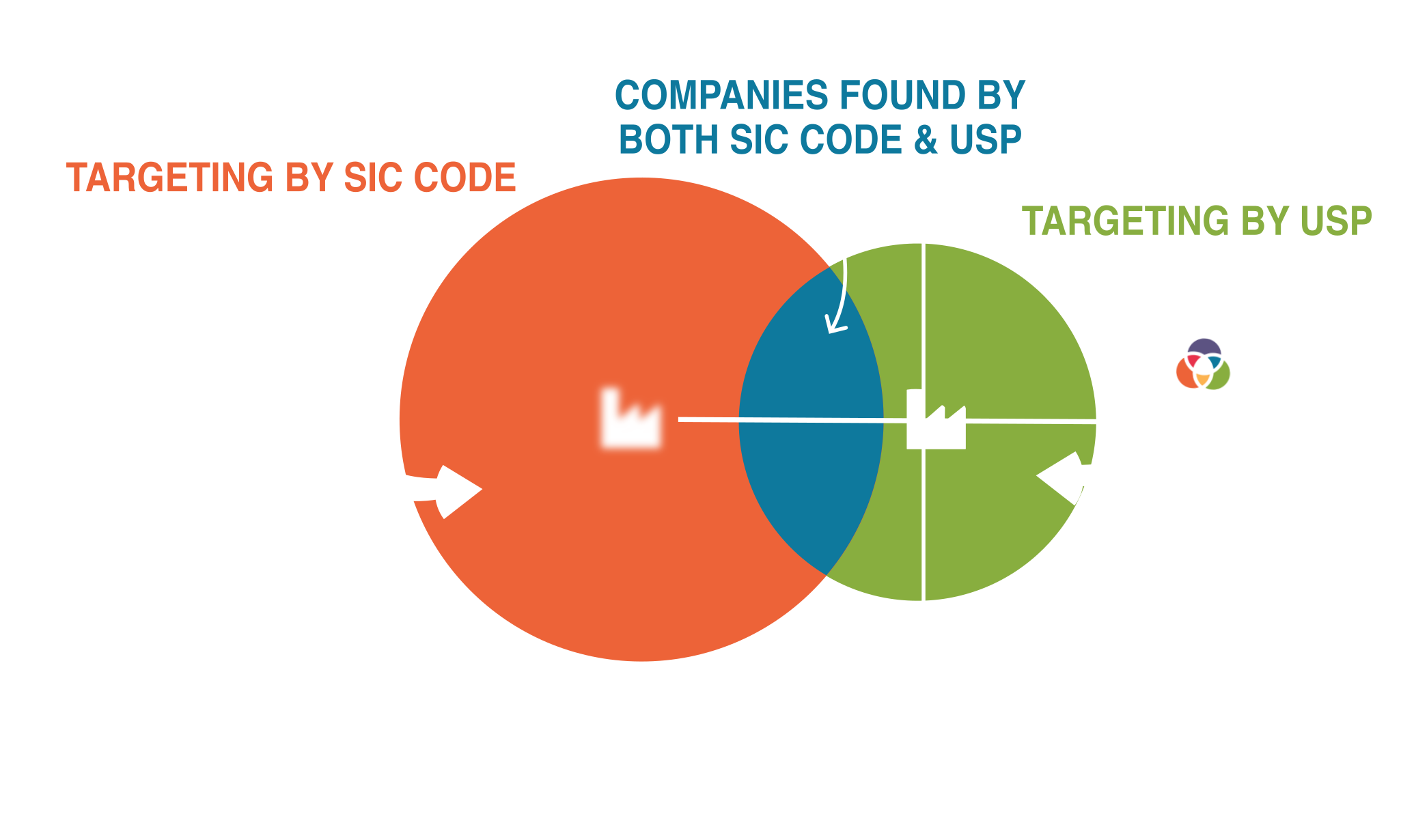

While Standard Industrial Classification (SIC) codes have traditionally served as a basis for industry classification, their limitations in accuracy, especially in a dynamic business environment, have become increasingly apparent. This article delves into the advantages of researched industry sector listings over SIC code classifications, with a focus on improving accuracy in classification. It examines how…

Continue reading...Find Company Information quickly with the USP Data App

Accelerating Deal Origination Deal Origination is made easier with the USP Data app. Because the universe of live UK companies is large we have included industry leading firmographic data selection tools to help you sift this mass of data to find company information you can rely on. The idea is that you can quickly screen…

Continue reading...Unveiling the Power of Niche Market Identification for Business Success

In a competitive SME business landscape, understanding and identifying relevant market niches is key. Of the 5 million plus limited companies live at Companies House there are probably only 1.7 million or so that are not dormant, intermediate holding companies or property management firms. This is still a considerable number to trawl through when attempting…

Continue reading...Converting your research to useful analysis

Just as a carpenter needs a saw in the toolbox to be taken seriously, anyone researching UK companies needs a tool like USP Data. Access to the latest information in an intuitive format is a pre-requisite if progress from research to analysis is to be swift. The definitive analysis of the list of suitable companies…

Continue reading...Shareholder Screening Guide

Shareholder profile can now be used as an additional screening criteria directly. SO the usual financial, geographic and sector seclections become subject to the selected shareholder profile such as age, and percentage of the shares. Using the templates you can extract the mailing addresses for the main shareholders for the shortlist of companies of interest…

Continue reading...Crm Upgrade Guide

The CRM has received a significant upgrade in the latest edition of USP Data. The CRM remains the best place to save your work. CRM projects can be viewed directly on the list view and exported or pushed through one of the new templates you are able to define. A big change is the manner…

Continue reading...Data Templates Guide

Templates are a new addition to USP Data. The idea is that any data displayed in the List View can be viewed or exported using a template which you can define to exactly suit your purposes: You can select the exact data of interest from USP Data You can order the columns in the template…

Continue reading...Find Firm Improvements Guide

The Find a Firm side tab which provides access to the latest information on all the live companies at Companies House has been improved by: Allowing the search returns to run to 10,000 records rather than just 300 Listing the SIC code report as well as the researched report in which each company is listed…

Continue reading...High Quality Keyword Search

Using keywords can be a great to identify the companies likely to be of interest. Of course the quality of the data being searched needs to be high and even then care needs to be taken if keyword searches are to result in useful suggestions. The latest update to USP focuses on adding powerful options…

Continue reading...Lead Building – sifting the wheat from the chaff

The sales funnel is a familiar concept which tracks the conversion of new contacts from suspects to leads to prospects and then to customers. This is typically represented as a cone with lots of leads being fed into the top of the cone and a much smaller number of customers resulting at the bottom. The…

Continue reading...Unlocking the opportunities hidden in abbreviated accounts

As you know Company Law allows “Small Companies” an option of disclosing less information at Companies House. This means that there is imperfect information in the public domain for SME firms. Companies House is the only verifiable source of financial data on privately held companies. As a result most of the attention is on the…

Continue reading...Valuing Companies Guide

Valuation is a tricky business! In a world of perfect information all risks are known, alternatives can be compared with certainty and cashflows can be discounted to provide the value of a firm. AI could be used to accurately land on a valuation which accounted for all the factors. It is clear that such perfect…

Continue reading...